class 8 trucks

forecasting

The first real signs that the truck freight market was shifting came last fall when spot rates for carriers – especially in dry van – began to outperform comparable rates in 2023 and 2024. Briefly, that strength appeared fleeting as the market cooled as usual after the holidays, but the big winter storm in the fourth week of this year led to sharply higher spot rates for both dry van and refrigerated.

The weather-induced spike isn’t unusual. What was different is that the settling from the spike was fairly gradual for refrigerated spot rates and nearly non-existent for dry van. In other words, the market appeared primed for an upward reset and just needed a catalyst, which it got. Flatbed spot rates were not affected, but they have continued to rise as we noted recently in our discussion of nonresidential construction.

The weather-induced spike isn’t unusual. What was different is that the settling from the spike was fairly gradual for refrigerated spot rates and nearly non-existent for dry van. In other words, the market appeared primed for an upward reset and just needed a catalyst, which it got. Flatbed spot rates were not affected, but they have continued to rise as we noted recently in our discussion of nonresidential construction.

This recent strength raises lots of questions, one of which is what higher spot rates mean for the for-hire carrier population, which seemed in recent months to settle at a level that is roughly 33% higher than it was before the pandemic – down from about 51% higher in late 2022 but still well beyond where the trendline would have taken the population had the pandemic never happened.

Complicating things, though, is the recent surge in diesel prices, which obviously will put enormous pressure on operations that are financially stressed. Four years ago, spot rates were falling – albeit from extraordinary high levels – when diesel prices surged following Russia’s invasion of Ukraine. Falling rates and surging fuel costs had an obvious impact on the market as many drivers gave up on their own authority and took jobs as employee drivers or leased owner operators. This time, rates are a positive while fuel is a negative, so the likely outcome is less of a no-brainer.

It might seem that tracking this is a simple matter, but it isn’t. We have fairly good insights into how many new carriers are coming into the market, but the data on carriers leaving the market takes time.

In general, a revocation of authority does not occur until about a month after an insurance company notifies the Federal Motor Carrier Safety Administration (FMCSA) that a trucking company no longer has insurance – and that could be weeks or perhaps even months after the trucking company actually stopped operating.

If we assume that the surge in diesel prices of more than $1.17 a gallon over the past two weeks resulted in a substantial number of carriers exiting the market, revocations of authority likely won’t start reflecting that until May or maybe even June.

FTR recently began tracking FMCSA’s notices of pending revocations, but even that data likely won’t show any change until at least late April. In the interim, we must rely on market signals, primarily spot rates.

Fortunately, we do have insights from multiple sources on the other side of the ledger.

One early indication of new entry is a business application – a step typically taken before a would-be owner-operator buys a truck or perhaps even applies with FMCSA for operating authority. The U.S. Census Bureau tracks applications for employer identification numbers (EINs), which is an early step in business formation.

The government data does not break applications down to the industry level; the closest relevant data is for transportation and warehousing. However, logically, the month-to-month changes in application levels would be driven mostly by trucking and, perhaps, secondarily by local delivery firms working for Amazon and others and storage businesses. We don’t see lots of applications for new airlines or railroads.

After a strong surge in January, applications pulled back in February. But even with that decline, activity remains meaningfully higher than it was a year ago and still elevated compared to most of the past couple of years.

So, the signs point to carrier creation, but, again, applying for an EIN is a long way from hitting the road with a truck and an MC number.

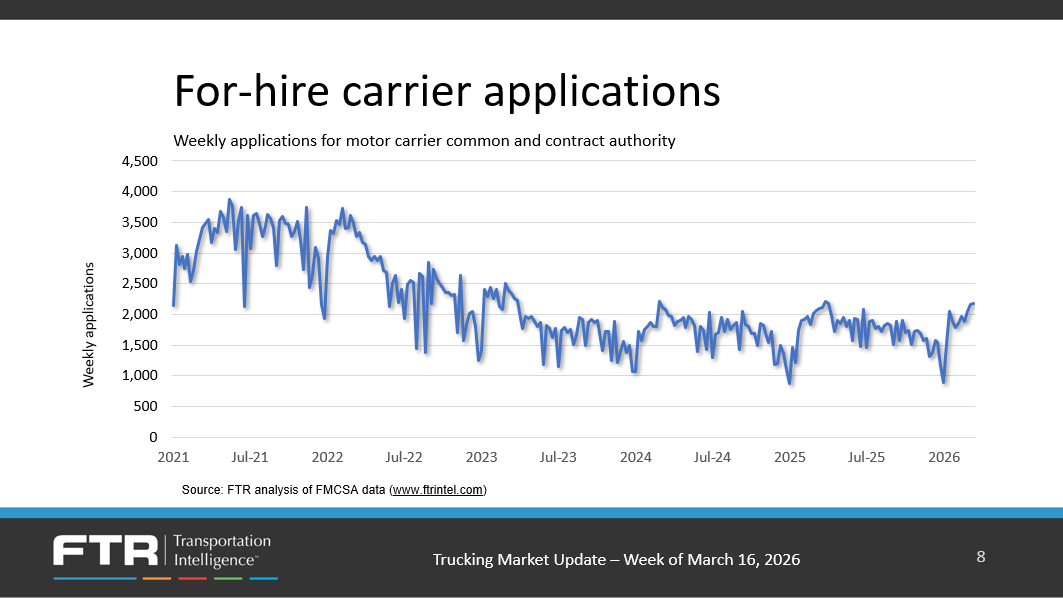

Authority Applications by Week

Authority Applications by WeekFTR has been tracking monthly applications (and revocations) of authority for more than five years. With the recent improvement in spot rates after three years of weakness, we have begun watching weekly figures for signs of any change in the market.

Applications for trucking authority rebounded quickly after the usual seasonal drop at the end of the year. In fact, they have climbed back to levels not seen since last spring, with momentum building over the past few weeks. The key question now is whether the unprecedented surge in diesel prices over the past couple of weeks will take the edge off applications. One reason to think that it might not is that recent spot rate gains have shown quite a bit of cost recovery for fuel – certainly compared to the 2022 experience when there was not cost recovery at all. Whether would-be carriers are thinking about it that thoroughly is an open question, though.

A point we emphasize constantly is that changes in the carrier population are not the same as changes in capacity because most of the carriers coming and going are essentially individual drivers moving between having their own authority on the one hand and being either company drivers or leased owner-operators on the other.

What the changes do indicate is whether a significant shift is occurring in the relationship between contract and spot. One reason that spot rates swing is that rate and capacity moves tend to work in concert. For example, the consumer stimulus and labor disruption in the spring of 2020 through winter of 2021 drove up spot rates which also lured many company drivers and leased owner-operators into the spot market as independent carriers. That dynamic further starved the contract market of capacity which – guess what? – drove even stronger spot activity.

Truckload carriers then worked hard to level the playing field and were having some modest success by late 2021, which began to soften the spot market. Then came the $1.15 diesel spike in two weeks and we already discussed what happened then. Contract capacity swelled, deflating the spot market even further.

Again, the near term is fuzzier because rates were beginning to favor operators in the spot market while soaring diesel costs are favoring larger carriers that have fuel surcharges with their customers.

The one missing element in a recovery for carriers is sustained freight volume growth. The industrial sector is beginning to show some signs of recovery, but it isn’t consistent. Meanwhile, there’s almost no growth in overall consumer spending and the more important spending on goods has been especially soft. Meanwhile, the housing sector continues to be weak with only flashes of promise.

While we wait for clarity in an economy clouded by tariffs and war, tracking carrier entry and exits will help us better understand how the market is interpreting all the conflicting forces.

.jpg?width=356&height=356&name=2026%20FTR%20Conference_SM_Trucking%20Market%20Insight(1).jpg)

Trucking leaders — mark your calendars.

The Truck Track at the 2026 FTR Transportation Conference returns!

📅 August 31 – September 1, 2026

📍 Indianapolis, IN

REGISTRATION OPENS APRIL1, 2026!

Sign up here to stay in the loop.