class 8 trucks

forecasting

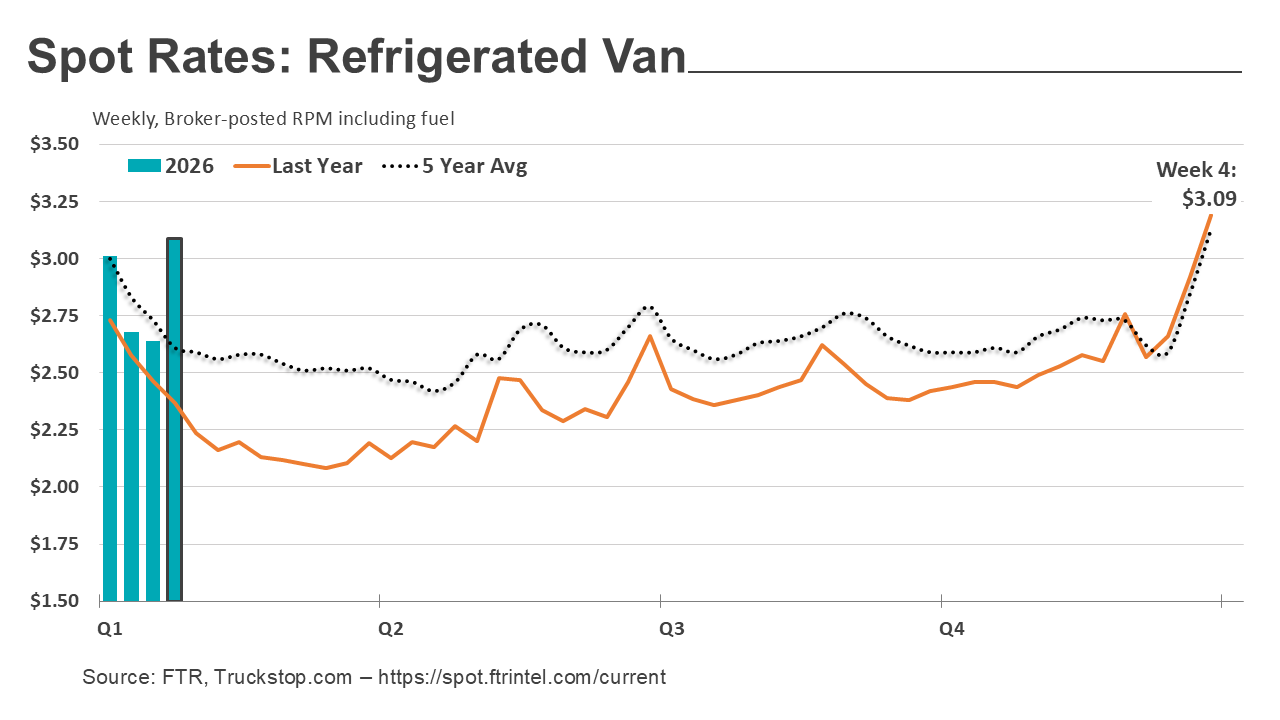

The first full week of February delivered one of the most dramatic spot market moves in recent years, driven less by underlying demand shifts and more by severe winter weather disruptions. In Episode 350 of FTR’s Trucking Market Update, the data tells a clear story: short-term shocks can still overwhelm seasonal patterns—at least temporarily.

Week 4 is typically a period of rate softness, but this year broke the mold.

Week 4 rate increases of this magnitude are historically rare. Over the past decade, both dry van and reefer rates almost always decline during this period.

Rates weren’t moving in isolation—volume confirmed the disruption.

The geographic concentration reinforces the weather narrative, with the Midwest and Northeast showing the largest increases in both rates and volumes.

For all the latest information on spot market rates go to https://spot.ftrintel.com/current

Despite the spot market volatility, carrier entry and exit data suggest a more stable underlying structure:

Despite the spot market volatility, carrier entry and exit data suggest a more stable underlying structure:

This balance suggests the recent rate surge is unlikely to immediately translate into a structural capacity shift—though March typically brings stronger new entry.

Fuel and operating costs are beginning to firm again:

Fuel and operating costs are beginning to firm again:

These cost pressures add another layer of complexity for fleets trying to interpret whether recent spot gains are opportunity-driven or purely reactive.

Outside trucking-specific indicators:

None of these signals point to an immediate demand inflection—reinforcing the idea that recent trucking volatility is event-driven rather than cyclical.

Episode 350 underscores a critical reminder for the freight market: short-term shocks can create extreme pricing signals without changing the underlying trajectory. The winter-driven surge in spot rates is meaningful, but it does not yet signal a sustained market reset.

FTR subscribers can track these developments in real time through the Trucking Update and Truck & Trailer Outlook reports. Together, they provide weekly insight into spot and contract market conditions, fleet capacity, equipment demand, production, and the macroeconomic forces shaping freight and equipment decisions over the next 24 months. Click on either image below to learn how these products can help your bottom line in 2026.